Understanding Global OTC Foreign Exchange (FX) Market

OTC FX Market is biggest market in the world. About 5.1 trillion USD are traded in this market every day.

Originally all FX transactions were for cross border trades in goods and services, but later on developments led to speculative investments activities in foreign currencies.

OTC FX Market is decentralized. It means there is no exchange on which currencies are traded. Interbank market in FX is among dealer banks. Dealer Banks are the biggest global banks. Top 10 banks who trade in FX have total trade volume of 67%.

USD is the dominant currency in global FX market. UK is the biggest location for FX trading followed by USA and Singapore. Hong Kong SAR and Japan are other important FX trading centers.

Markets operate 24/7 unlike other financial markets which open and close at certain times.

Bank of International Settlement publishes its triennial survey of global FX markets. 2016 survey showed 5.1 trillion USD/day FX turnover down from 5.3 T/Day back in 2013 survey. Markets peaked in September of 2014 at 6.5 Trillion USD/day. Since then the trend is declining. De-risking by global banks, decline in global trade are cited as main reasons for decline. Will attempt to understand this issue at a later date.

Following Issues emerge from this post but are not discussed here in detail.

- Retail FX Market

- Algorithmic Trading

- Non Bank High Frequency Liquidity Providers

- FX Prime Brokerage

- Financial Stability in OTC Market – Case for CCP

- China RMB Internationalization

- Clearing and Settlement in FX Markets – CLS Bank and CLSNet

- Liquidity for FX trades – Funding and Market Liquidity

Highlights from the 2016 Triennial Survey of turnover in OTC foreign exchange markets:

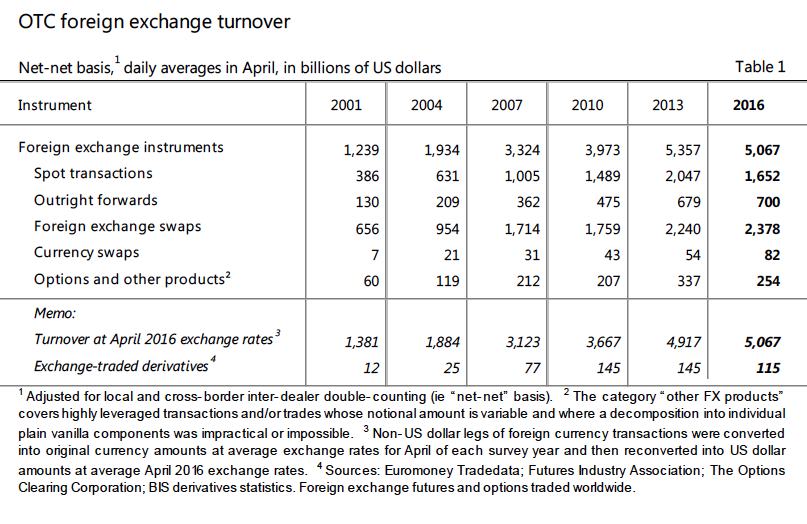

- Trading in foreign exchange markets averaged $5.1 trillion per day in April 2016. This is down from $5.4 trillion in April 2013, a month which had seen heightened activity in Japanese yen against the background of monetary policy developments at that time.

- For first time since 2001, spot turnover declined. Spot transactions fell to $1.7 trillion per day in April 2016 from $2.0 trillion in 2013. In contrast, the turnover of FX swaps rose further, reaching $2.4 trillion per day in April 2016. This rise was driven in large part by increased trading of FX swaps involving yen.

- The US dollar remained the dominant vehicle currency, being on one side of 88% of all trades in April 2016. The euro, yen and Australian dollar all lost market share. In contrast, many emerging market currencies increased their share. The renminbi doubled its share, to 4%, to become the world’s eighth most actively traded currency and the most actively traded emerging market currency, overtaking the Mexican peso. The rise in the share of renminbi was primarily due to the increase in trading against the US dollar. In April 2016, as much as 95% of renminbi trading volume was against the US dollar.

- The share of trading between reporting dealers grew over the three-year period, accounting for 42% of turnover in April 2016, compared with 39% in April 2013. Banks other than reporting dealers accounted for a further 22% of turnover. Institutional investors were the third largest group of counterparties in FX markets, at 16%.

- In April 2016, sales desks in five countries – the United Kingdom, the United States, Singapore, Hong Kong SAR and Japan – intermediated 77% of foreign exchange trading, up from 75% in April 2013 and 71% in April 2010.

Interbank (OTC) Market Infrastructure and Institutions

- Banks

- Non Banks

- Exchanges

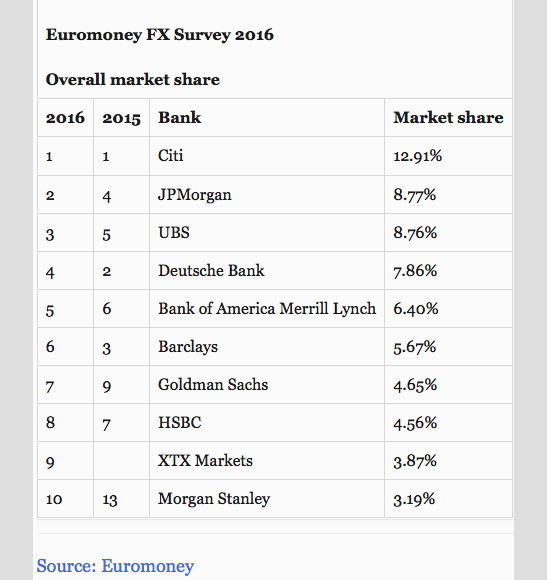

Top 10 Banks in FX

From All change in the 2016 Euromoney FX rankings

Citi holds on to the top ranking in this year’s Euromoney foreign exchange rankings, but elsewhere there have been unprecedented shifts.

Structural changes to the markets, management upheaval among many big banks, new non-bank entrants and lack of volumes and volatility have seemingly levelled the playing field among the industry’s biggest firms.

The biggest change in the rankings this year is the decline of the combined market share of the top five global banks. Their market share in the survey peaked in 2009 at 61.5% and was still above 60% as recently as 2014.

This year the top five banks account for just 44.7% of total volume. The hopes of many global FX heads and their investment bank bosses – that the share of the big banks would rise inexorably as the market became more automated and that they would be able to benefit from oligopolistic pricing power as a result – now seem like distant and deluded dreams.

One FX veteran tells Euromoney that the decline of the top five banks’ combined market share “is exactly what the regulators would want in a market they continue to keep a very close eye on.”

While the market share of the top 10 FX houses overall also declines, from over 75% last year to just 66% this year, the fall is entirely due to the performance of the top five banks. The banks ranked from sixth to 10th place overall produced a combined market share of 22%, roughly in line with the last five years of the survey and considerably higher than the 14% they managed in 2008.

Citi actually extends its lead over the second-placed bank in the survey, which market participants regard as the most accurate reflection of client-based activity in the global foreign exchange markets, to more than four percentage points – even though the bank’s own market share declined by more than three percentage points, from 16.11% in the 2015 survey to 12.91% of trading in 2016.

That winning market share is the lowest for any top-ranked bank in the survey since UBS won the survey in 2004.

Citi maintained its leadership overall in important product areas such as spot/forwards and swaps, as well as in the key real money and bank client categories. It rises one place this year to win in corporates and overall electronic market share, although it falls to third overall for options.

One big story in this year’s rankings is the decline of Deutsche Bank. It was once the undisputed leader in global foreign exchange, losing the top position in the Euromoney rankings three years ago after nearly a decade of dominance.

While new group CEO John Cryan has gone out of his way both publicly and privately to describe the FX business as one of the beleaguered bank’s crown jewels, the days when Deutsche Bank was able to secure an overall market share of more than 20% (as recently as 2009) are long gone.

In the latest set of rankings, Deutsche falls from second to fourth place overall: its market share of 7.86% is almost half what it was a year ago. Deutsche’s decline is widespread, and competitors say has been driven in part by the bank cutting back on the number of clients it covers. It falls from second to fifth in spot/forward; from second to eighth among real money clients and loses top spot among bank clients. It remains the leading overall options house.

Perhaps the most surprising fall of all is in its overall electronic market share. Deutsche’s Autobahn system revolutionized global FX trading and in banner years accounted for more than a quarter of all electronic trading. This year, Deutsche can only manage fourth place in e-market share, from holding the top ranking last year, and its share has fallen from 17.5% to 8.73%.

Two banks overtake Deutsche to move into the top three overall, but the similarities end there: the two banks in question have very different recent histories in global foreign exchange.

JPMorgan jumps to second place in the survey, with a market share of 8.77%, up from fourth place with 7.65% last year. For many years, competitors have said that JPMorgan has failed to punch its weight in FX; it has typically ranked outside the top five overall banks in the Euromoney survey for the last decade. Those accusations have less weight now, even though they have been replaced by rumours about the bank’s competitive pricing strategy.

The US bank rises across a range of categories. Its most notable successes are winning the leveraged fund category with a lead over second-placed UBS of almost eight percentage points and a market share of more than 18%; and jumping from fifth to second place in overall electronic trading. JPMorgan’s one poor ranking is now in options, where it comes a lowly eighth.

UBS returns to the top three global FX banks overall this year. A winner back in 2004, it has been outside the top three since 2009, and last challenged for the top spot overall a year earlier, when its market share of almost 16% was only beaten by Deutsche. Last year it fell to fifth place, its worst performance in a decade, with a market share of 7.3%.

Given the bank’s leadership has spent the last few years de-emphasizing the role of its investment bank, some competitors believed UBS was on a long, slow decline in FX.

But, quietly and consistently, UBS’s markets business has been recalibrating to the new capital and markets environment, as well as maintaining a commitment to best-in-class electronic platforms. Its overall market share rises to 8.76%; and it breaks into the top three overall in spot/forward, swaps, electronic market share and for bank clients. Like JPMorgan, it is a laggard in options, where it ranks seventh.

JPMorgan and UBS have one other important thing in common: while other banks have lost entire benches of senior management from their FX teams in recent years, JPMorgan and UBS have been relatively stable.

At the former, Troy Rohrbach has overseen the FX business since 2005 (he now also runs rates and public finance globally); at UBS, Chris Murphy and George Athanasopoulos, the global co-heads of FX, rates and credit, both joined the bank more than five years ago and have jointly run the division since 2013. Leadership, it seems, does count.

Bank of America Merrill Lynch continues its steady rise up the rankings of recent years, from a nadir of 12th place from 2009 to 2012. It finally breaks into the top five global FX houses overall, up from sixth place last year.

BAML jumped up the rankings into the top five for corporates and real money accounts, and gained ground in both swaps and options – in the latter, it ranks second globally. But BAML still has work to do in the electronic market, where its overall ranking fell from sixth to seventh place. Other US banks also performed well.

Goldman Sachs rose from ninth to seventh overall and Morgan Stanley jumped three places to break back into the top 10.

It has not been a good year in FX for Barclays. Perhaps the bank’s decision to not have a global head of foreign exchange has backfired. The UK-cum-transatlantic bank dropped from third place overall to sixth, and its market share from 8.11% to 5.67%.

Barclays slipped three places to seventh in spot/forward, four places to seventh in swaps and three places to ninth in options. Among client groups, its biggest reversal came among real money accounts, falling from fourth place last year to outside the top 10.

HSBC has also had a disappointing year, falling from seventh to eighth place overall. It also loses its top ranking among corporates last year, falling out of the top five of that client category altogether. Electronic trading remains the bank’s weakest link, and may even be getting weaker, as the bank falls to ninth place in overall e-market share.

New phenomenon

Banks have always risen and fallen in the Euromoney rankings over the last 40 years, but this year sees a new phenomenon – the advent of the non-bank liquidity provider. Leading the way is XTX Markets, a spin-off of GSA Capital, whose co-CEO Zar Amrolia was a frequent winner of the Euromoney FX rankings in his previous role as head of Deutsche Bank’s FX business.

In its first year of eligibility, the spot-only XTX makes a stunning debut: ninth place in the overall rankings with a market share of 3.87%; fourth in spot/forwards; fifth for bank clients; third for FX trading platforms; fifth overall for e-market share; and third for electronic trading of spot, ahead of Deutsche Bank with a market share of more than 10%.

XTX is the leader, but not the only non-bank entrant to the survey. Tower Research Capital, Jump Trading, Virtu Financial, Lucid Markets and Citadel Securities all make the top 50 overall market share rankings.

XTX’s ninth place overall looks like a line in the sand for the FX markets. The banks above it are, for the most part, the remaining price-makers; the banks below often price-takers, with the ability to make markets in particular currencies or products.

Many of the banks ranked outside the top 10 overall this year are understood to be sourcing liquidity from non-bank providers such as XTX, Tower and Jump. They look set to gain more market share in the future, helped by new technology, more defined business models and a lower-cost infrastructure base than the traditional FX banks. They could look to build capability in forwards and other markets in the near future.

Among multi-dealer platforms, Thomson Reuters – through its FXall service – remains the clear leader with a 30% market share, although its margin over second-ranked FXConnect almost halved. The big riser among MDPs was third-ranked HotspotFXi, which increased its market share from less than 7% to almost 18% this year.

Total volumes in the Euromoney FX survey came in at almost $95 trillion, while the number of votes held steady compared with last year at around 3,500 clients. That represents a volume fall of around 23% on last year, in line with market expectations.

Electronic FX platforms

There are three types of trading platforms.

- Interdealer

- Multidealer

- Singledealer

Trading platforms can be divided into three different types:

- Inter-dealer electronic broking platforms. These platforms were developed in the 1990s and are regarded, according to the Bank for international Settlements (BiS, 2010), as the dominant source of interbank liquidity on the foreign exchange market. They mediate information on various market makers’ indicative prices. EBS and Reuters, based in London, are the two dominant platforms within this category.

- Multi-bank platforms. These platforms are also known as multi-bank ECNs (electronic communication networks). They were created in the first decade of this century and resemble the previous category in that they mediate several market makers’ prices. one difference is that they have freer access regulations for market makers, which makes it easier for market makers to join these platforms. Another difference is that they are largely used outside the interbank market, which is to say by market participants that are not banks. The US platforms Fx All, currenex, Hotspot Fx, State Street and Fx connect are examples of this type of trading platform. There are also platforms that provide standardised algorithmic trading functions as a service. currenex is one such platform.

- Single-bank platforms. This type of platform is run by an individual bank. The platform mediates only the individual bank’s own prices for various currency pairs, unlike the trading platforms discussed above, which mediate several market makers’ prices. in Sweden, SeB has a platform of this type, SeB Trading Station. other examples of banks with such platforms are JP Morgan, Deutsche Bank and citibank.

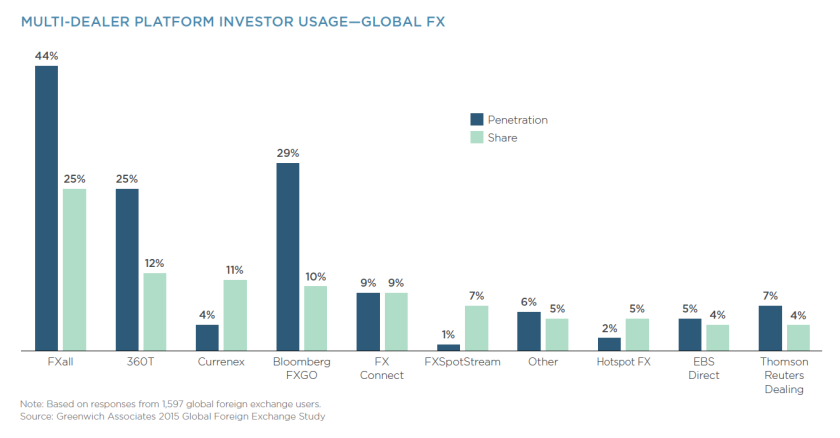

A. Multi Dealer Platforms

J.P. Morgan has significantly increased its footprint on these platforms over the past couple of years and now ranks first for penetration globally, followed closely by Citi. Bank of America Merrill Lynch, Deutsche Bank and HSBC round out the top five most prominent banks on MDPs.

B. Single Dealer Platforms

While multi-dealer systems are clearly on the rise, an average of more than 20% of trading volume of banks and hedge funds is still executed on single-bank platforms. Barclays, Citi and Deutsche Bank are the clear top three most actively used single-dealer platforms globally.

“Proprietary platforms give banks a means of retaining profitable trading volumes, so dealers are expanding these systems to provide a range of liquidity choices that enable clients to access the market in a variety of ways, including disclosed and non-disclosed liquidity, agency and principal trades, and links to exchange-based execution,” says Greenwich Associates Managing Director Woody Canaday.

C. Algorithmic Trading

Dealers are also in the early days of what promises to be an all-out arms race in algorithmic trading. Currently only 13% of top-tier FX customers use algorithmic trading models. However, that share approaches one-quarter among the market’s biggest buy-side participants and 30% among hedge funds.

Two trends suggest that algorithmic trading is gaining traction in FX. First, market participants that use algo-rithmic models are tapping an expanding number of dealers for algorithms. Second, current users are routing growing shares of trading volume through the models, from 25% in 2014 to 28% in 2015. Hedge funds that trade algorithmically now use these models for about half of total trading volume.

A. Inter-dealer electronic broking platforms

- Reuters Dealing 3000

- ICAP EBS

EBS is the primary trading venue for EUR/USD, USD/JPY, EUR/JPY, USD/CHF, EUR/CHF and USD/CNH.

Thomson Reuters Matching is the primary trading venue for commonwealth (AUD/USD, NZD/USD, USD/CAD) and emerging market currency pairs.

ICAP EBS

EBS was created by a partnership of the world’s largest foreign exchange (FX) market making banks in 1990 to challenge Reuters’ threatened monopoly in interbank spot foreign exchange and provide effective competition. By 2007, approximately US$164 billion in spot foreign exchange transactions were traded every day over EBS’s central limit order book, EBS Market.

EBS’s closest competitor is Reuters Dealing 3000 Spot Matching. The decision by an FX trader whether to use EBS or Thomson Reuters Matching is driven largely by currency pair. In practice, EBS is the primary trading venue for EUR/USD, USD/JPY, EUR/JPY, USD/CHF, EUR/CHF and USD/CNH, and Thomson Reuters Matching is the primary trading venue for commonwealth (AUD/USD, NZD/USD, USD/CAD) and emerging market currency pairs.

EBS initiated e-trading in spot precious metals, spanning spot gold, silver, platinum and palladium, and remains the leading electronic broker in spot gold and silver through the Loco London Market.

They were the first organisation to facilitate orderly black box or algorithmic trading in spot FX, through an application programming interface (API). By 2007 this accounted for 60% of all EBS flow.

In addition to spot FX and Precious Metals, EBS has expanded trading products through its venues to include NDFs, forwards and FX options. It has also increased the range of trading style to include RFQ and streaming in disclosed and non-disclosed environments.

EBS was acquired by ICAP, the world’s largest inter-dealer broker, in June 2006. ICAP said that the acquisition would combine EBS’ strengths in electronic spot foreign exchange with ICAP’s Electronic Broking business to create a single global multi-product business with further growth potential and significant economies of scale. It went on to say that would provide customers with more efficient electronic trade execution, reduced integration costs and give access to broad liquidity across a wide product range.[1]

In 2014, EBS merged with BrokerTec – a leading service provider in the fixed income markets – to form EBS BrokerTec. BrokerTec’s offering comprises trading solutions for many US and European fixed income products including US Treasuries, European Government Bonds and European Repo.

EBS BrokerTec is now recognised as a market-leading e-trading technology and solutions provider, offering access to multiple execution options and diverse, valuable liquidity across the FX and fixed income markets.

- ICAP EBS is one of the world’s premier inter-dealer brokers with average daily transaction volume in excess of USD 2.3 trillion.

- ICAP’s electronic EBS platform provides the primary market of natural interest for more than 2800 global FX, Precious Metals and NDF traders.

- ICAP EBS global access platform delivers anonymous, transparent and reliable FX Liquidity.

- Authoritative real-time and historical market data.

- Available for clearing only. Relationship with EBS required.

B. Multidealer Platforms – FX ECNs

Since 1999, banks have been developing proprietary systems for their customers to trade foreign exchange and access research material over the internet. To trade with multiple banks online, customers therefore need to use a variety of authentication methods, websites and price request methods. Multi-bank platforms have evolved to allow customers to use a single website to request prices simultaneously from multiple banks and view research material online. Multi-bank platforms (also known as ECNs or electronic communication networks) offer significant advantages to customers, but fewer advantages to banks, and therefore active participation by banks in multi-bank platforms is driven largely by customer demand. However, for the banks it remains preferable for their customers to trade through bank proprietary systems as the banks avoid paying brokerage and customers are encouraged to focus only on the particular bank’s prices.

There are five main customer-facing FX ECNs:

FXall – founded by Bank of America, Credit Suisse First Boston, Goldman Sachs, HSBC, JP Morgan, Morgan Stanley Dean Witter and UBS

Currenex – independent and venture backed by major market participants, e.g. Barclays Capital and Royal Dutch/Shell

FX Connect – owned by State Street

360T – independent and venture backed by financial and major private investors

Hotspot FXi – independent privately held venture capital-backed company

Currency Trading Shifts to Multi-Dealer Systems, Greenwich Says

Lananh Nguyen

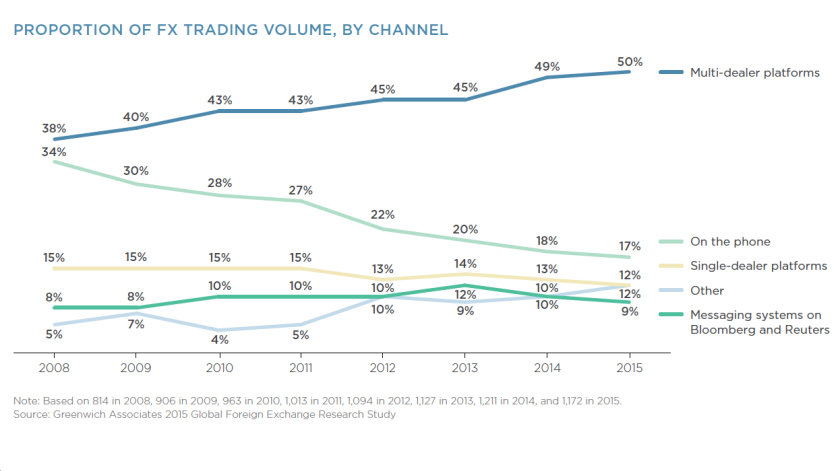

July 14, 2015, 11:28 AM EDTCurrency investors are increasingly using electronic systems connected to multiple dealers as the market comes under greater scrutiny by regulators, according to Greenwich Associates.

Institutional investors and large corporations executed 49 percent of their foreign-exchange trading volumes on multi-dealer platforms last year, up from 45 percent in 2013 and 38 percent in 2008, the Stamford, Connecticut-based consultant said in a report. The increase comes as trading by traditional methods, such as phone, instant messaging and single-dealer platforms, has fallen.

“The FX ‘fixing scandal’ and related bank fines have already played a part in changing buy-side behavior,” wrote Kevin McPartland, head of research for market structure and technology at Greenwich, who co-authored the report based on interviews with more than 1,600 people participating in foreign-exchange markets globally.

Asset-management companies are boosting electronic trading as regulatory scrutiny discourages banks and dealers from providing “market color” to clients to avoid any perception of impropriety, according to Greenwich. The platforms are also becoming more popular as banks become less active in currency markets because of rising capital requirements.

“Asset managers have proactively worked to beef up internal policies to both ensure maximum returns for the impacted funds and to reassure customers, such as pension funds and sovereign wealth funds, that they’re getting the best the market has to offer at that moment in time,” McPartland wrote.

Thomson Reuters Corp.’s FXall platform had the largest volume-weighted share of trading last year at 21 percent, according to Greenwich. It’s followed in popularity by 360T, State Street Corp.’s Currenex, Bloomberg LP’s FXGO and FX Connect.

Dealer-to-client platforms

- State Street FX Connect

- Thomson Reuters FXall

- State Street Currenex

- CBOE/BATS Hotspot FX

- Bloomberg FXGO

C. Single Dealer FX Trading Platforms

- Barclays BARX

- Citi Velocity

- Deutsche Autobahn

- Morgan Stanley Matrix

- UBS Neo

Best Single-Dealer FX Trading Platform

Financial News is delighted to announce the . The winners will be announced at a gala dinner in London in October.

Here are the nominees in the category of Best Single-Dealer FX Trading Platform:

Barclays BARX

The BARX platform remains a dominant force among single-dealer platforms, with streaming prices in more than 80 currencies and 480 currency pairs, with a wide range of products available. Following the launch of BARX Gator, a liquidity aggregator, Barclays now gives clients access to the increasingly popular agency-style of execution.Citi Velocity

Since its relaunch in 2012, Citi Velocity 2.0 has become a leading source of single-bank liquidity in FX cash, options and rates trading. Citi has also led the adoption of mobile and tablet technology in this space, and has focused its efforts with Velocity on delivering speed, lower transaction costs, cross-asset information, cross-asset trading, deep liquidity, and desktop efficiency.Deutsche Bank Autobahn

Deutsche Bank has channelled significant resources into its electronic trading franchise in recent years, and Autobahn remains a major player across asset classes. In FX, Autobahn provides a single blotter for trades executed via both voice and electronic channels. Users can thus benefit from a combined view and take greater control over their portfolios.Morgan Stanley Matrix

While not a top-tier bank in FX, Morgan Stanley has sought to add unique value with its Matrix platform. That has been achieved in part through execution and post-trade services, but also through the bank’s quantitative solutions and innovations group, which develops unique analytical tools to help users make more informed trading and investment decisions.UBS Neo

Launched in 2013, UBS Neo is a cross-asset class platform providing a single point of access with a strong user experience, re-establishing the Swiss bank as a significant player in electronic trading. UBS Neo FX covers 550 currency pairs, with access to cash, NDFs and options available through the platform.

Trends in use of Electronic Platforms

From The $4 trillion question: what explains FX growth since the 2007 survey?

Electronic execution methods are transforming the FX market The greater activity of all three of the above-mentioned customer types – highfrequency traders, banks as clients and retail investors – is closely related to the growth of electronic execution methods in FX markets. Greenwich Associates estimates that more than 50% of total foreign exchange trading volume is now being executed electronically (Graph 3, left-hand panel).

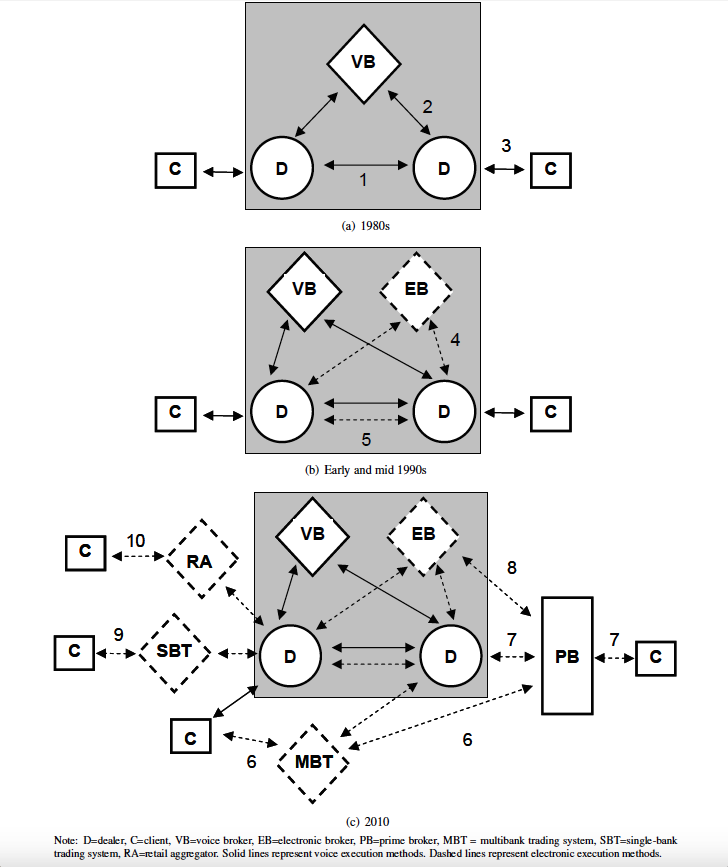

Electronic execution methods can be divided into three categories: electronic brokers, multi-bank trading systems and single-bank trading systems. Electronic brokers were introduced in the inter-dealer FX market as early as in 1992. For customers, however, the main channel for trading continued to be direct contact with dealers by telephone. In the rather opaque and fragmented FX market of the 1990s, barriers to entry were high and competition was limited. Customers typically paid large spreads on their FX trades.

The first multi-bank trading system was Currenex, which was launched in 1999. By providing customers with competing quotes from different FX dealers on a single page, Currenex increased transparency, reduced transaction costs and attracted a growing customer base. State Street’s FXConnect, which had been launched in 1996 as a single-bank trading system servicing only State Street’s clients, opened up in 2000 and became a multi-bank ECN.

In response to the increased competition, top FX dealers launched proprietary single-bank trading systems for their clients, such as Barclays’ BARX in 2001, Deutsche Bank’s Autobahn in 2002 and Citigroup’s Velocity in 2006. According to data provided to the BIS, daily average trading volumes on the top single-bank trading systems have increased by up to 200% over the past three years.

Market Participants in

- Interbank Market

- Retail Market

Forex Market Players

Forex Market

The Forex market is an international over-the-counter market (OTC). It means that it is a decentralized, self-regulated market with no central exchange or clearing house, unlike stocks and futures markets. This structure eliminates fees for exchange and clearing, thereby reducing transaction costs.

The Forex OTC market is formed by different participants – with varying needs and interests – that trade directly with each other. These participants can be divided in two groups: the interbank market and the retail market.

The Interbank Market

The interbank market designates Forex transactions that occur between central banks, commercial banks and financial institutions.

Central Banks – National central banks (such as the US Fed and the ECB) play an important role in the Forex market. As principal monetary authority, their role consists in achieving price stability and economic growth. To do so, they regulate the entire money supply in the economy by setting interest rates and reserve requirements. They also manage the country’s foreign exchange reserves that they can use in order to influence market conditions and exchange rates.

Commercial Banks – Commercial banks (such as Deutsche Bank and Barclays) provide liquidity to the Forex market due to the trading volume they handle every day. Some of this trading represents foreign currency conversions on behalf of customers’ needs while some is carried out by the banks’ proprietary trading desk for speculative purpose.

Financial Institutions – Financial institutions such as money managers, investment funds, pension funds and brokerage companies trade foreign currencies as part of their obligations to seek the best investment opportunities for their clients. For example, a manager of an international equity portfolio will have to engage in currency trading in order to buy and sell foreign stocks.

The Retail Market

The retail market designates transactions made by smaller speculators and investors. These transactions are executed through Forex brokers who act as a mediator between the retail market and the interbank market. The participants of the retail market are hedge funds, corporations and individuals.

Hedge Funds – Hedge funds are private investment funds that speculate in various assets classes using leverage. Macro Hedge Funds pursue trading opportunities in the Forex Market. They design and execute trades after conducting a macroeconomic analysis that reviews the challenges affecting a country and its currency. Due to their large amounts of liquidity and their aggressive strategies, they are a major contributor to the dynamic of Forex Market.

Corporations – They represent the companies that are engaged in import/export activities with foreign counterparts. Their primary business requires them to purchase and sell foreign currencies in exchange for goods, exposing them to currency risks. Through the Forex market, they convert currencies and hedge themselves against future fluctuations.

Individuals – Individual traders or investors trade Forex on their own capital in order to profit from speculation on future exchange rates. They mainly operate through Forex platforms that offer tight spreads, immediate execution and highly leveraged margin accounts.

Trend Towards Exchanges ?

Only 200 billion daily turnover using exchanges

Exchanges are staking out the $5tn a day global currency market as part of their latest efforts to tap this lucrative and booming sector that has long been dominated by global banks.

This week Bats Global Markets, the US’s second largest equities exchange, fired the latest salvo by offering three months of free trading on its forthcoming London-based Hotspot currency trading platform, the centrepiece of Bats’ $365m purchase of the venue from KCG Holdings in March.

That came only days after Deutsche Börse, Europe’s largest exchanges operator, bought 360T, one of the world’s largest currency trading networks, for €725m.

Their moves are audacious attempts to break into the world’s most liquid over-the-counter market, where a notional $5.3tn a day is traded in cash, or spot, and derivatives trades. It is dominated by banks, which continue to make billions of dollars in profits from it each year. Exchanges have generally been unable to establish a presence in this and other OTC markets, despite repeated attempts to do so.

In currencies, Chicago’s CME Group dominates futures trading, reflecting how it seized the terrain in the 1970s when the present era of floating foreign exchanges began. Markets in Moscow, Brazil and India also trade local currency, but of that $5.3tn total, global exchanges account for just $200bn according to Aite Group, a financial markets consultancy.

However, cracks are appearing in the market edifice, brought on by a combination of unlawful activity by banks, deep structural change and the emergence of cheap and reliable technology that has allowed alternative ways of trading to emerge.

“The banks as a whole will continue to have a substantial piece of the pie but the regulations will force them to let go of pieces of it,” says Javier Paz, an analyst at Aite Group.Waves of post financial crisis regulation have accelerated change in equity and interest rate swaps markets, but global policymakers largely left the currency market alone.

However, the currency industry is mopping up after two of its own existential crises — the Wm/Reuters benchmark rate rigging scandal, which resulted in multibillion-dollar fines for banks, and the sudden move by the Swiss franc in January when the national central bank abolished its ceiling against the euro.

Market observers say that end users such as corporations, hedge funds and asset managers are now taking far more care with their orders, and they have the tools to do it, turning the banks more into agency brokers.

“End users are getting used to technology where they have a full view of the market. They are accessing more markets than they could ever do 10 years ago,” says Chris Concannon, chief executive of Bats Global Markets.

At the same time, incidents like the Swiss move have also raised the alarm among banks. By the end of that day in January some smaller retail brokers faced ruin but even several larger broker-dealers such as Barclays, Citigroup and Deutsche Bank nursed tens of millions of dollars in losses. That has also left the market seeking as many different venues as possible where they can offset their customers’ trades.

“People are not holding risk like they were a year ago. A year ago they would warehouse that risk and wait for another customer to come along,” says Mr Concannon.Not helping matters is how foreign exchange market liquidity is highly concentrated among just a handful of trading pairs, known as the G10. Into the gap on the other side of the trade are stepping high-frequency traders such as the US’s Virtu Financial. It is one of the world’s largest currency market makers.

“Clients that are trading on anonymous platforms by definition have no insight into whom they are trading with, and as such are likely interacting with non-bank liquidity providers more often than they know,” notes a report by Greenwich Associates last month.

However, even if the diagnosis is right, exchanges still face tough competition from well-established platforms not run by banks, such as Thomson Reuters, Bloomberg FXGO and ICAP’s EBS. These make up the majority of the $1.1tn average daily volume traded on electronic FX platforms and provide a role as a more centralised price benchmark independent of banks.

Bats, which has targeted London because it is the world’s main location for forex trading, will aim to provide a reliable venue for pricing and take more trading volume from the 220 banks, asset managers, hedge funds, dealers and retail brokers signed up to the venue.

Deutsche Börse sees 360T as a key part of its growth strategy, using it as a way to sell market data and develop futures, FX forwards and swaps trading to boost its Eurex derivatives business. But it is trading network, not an exchange-like central limit order book.

Critically, OTC markets are historically highly resistant to encroachment from exchanges and some see little sign of that changing.

The head of one currency trading platform says: “I don’t see any signs of moving to an exchange model. I don’t see a slam dunk here, I see some desperate buyers looking for a growth story.”

OTC FX trading becomes ‘exchange-like’

Thursday, April 21, 2016

The acquisition of trading platforms Hotspot and 360T by Bats Global Markets and Deutsche Börse respectively last year were bold statements of intent by exchange operators to grab a larger chunk of the trillions of dollars traded in FX every day.

FXSpotStream

However, while consolidation in the venues supporting FX trading can be expected to result in exchanges becoming more involved in the FX space, any actual market structure change is likely to take a long time to materialize, according to

FXSpotStream CEO Alan Schwarz.

“The FX market continues to do a good job of addressing regulatory requirements and meeting the demands of market participants,” he says.

“We have seen a shift in the FX market looking to trade more on a disclosed basis. Our business has continued to see year-on-year growth because there is a move taking place from exchange-like anonymous trading to bilateral, fully disclosed trading between counterparties.

“Unlike trading on an exchange, the relationship via FXSpotStream is transparent and trading with the liquidity providing banks is on a fully disclosed basis.”

Nuances

Kevin McPartland, head of market structure and technology research at Greenwich Associates, believes that discussion of migration from OTC to exchange fails to take account of some of the nuances of the FX market and that the future lies in venues that support multiple trading models.

“There are a host of non-exchange electronic trading venues that allow clients to trade with each other in a variety of ways,” he says.

Kevin McPartland,

Greenwich AssociatesOn the question of whether there is a discernible shift towards fully disclosed trading, McPartland refers to both central limit order book (CLOB) and request-for-quote (RFQ) having their merits.

Despite observations made by the likes of TeraExchange – that order book platforms offer a democratic marketplace through transparent, firm and executable prices – corporates have remained reluctant to abandon the RFQ model.

The key question for CLOB platform providers continues to be not why market participants have migrated to alternative models but rather when they will be in a position to win new business for products that are most suited for order books, such as the benchmarks and plain vanilla products.

“RGQ offers liquidity on demand and identification of counterparties, whereas CLOB is faster and its anonymity can be helpful,” says McPartland.

“But we are now seeing demand for a solution that provides the best of both worlds by enabling trading in an order book format while maintaining a bilateral relationship with counterparties.”

Regulation

According to James Sinclair, CEO of MarketFactory, options and other derivatives are moving closer to an exchange model due to the direct effects of regulation and the increased costs of compliance in OTC markets.

He refers to CME FX options as an example, noting they are effectively options on futures.

“However, the situation in the spot market is more complicated – some aspects are becoming closer to an exchange, others are moving further away,” he says. “FX has its own market structure that is hard to fit into the OTC/exchange paradigm.”

James Sinclair,

MarketFactoryOne of the fundamental reasons why the market does not become centrally cleared, says Sinclair, is that a cleared model carries the cost of insurance against both settlement and market risk.

“CLS insures you against settlement risk but not the market risk,” he adds. “Counterparts still find it cheaper to self-insure against market risk in case of a counterparty default than to pay the extra cost of a fully cleared solution.”

A senior platform source observes that growth in exchange-traded products has largely come from futures traders who have looked for diversification and added FX as another asset class.

“Very little business has moved from OTC – some banks have added exchanges as additional liquidity sources to cover risk, but that is really the only business that has crossed the divide,” the source says.

OTC has become more exchange-like in that the largest banks have continued to extend their internalization of flow, so each now runs an order book trading structure internally.

However, our source also points out that the tightening of credit has reduced the number of prime brokers in FX and costs have risen “so the nearest thing that the FX OTC market has to centralized clearing has actually reduced its volume and capacity”, he concludes.

Evolution of Information Exchange in Trading Platforms

- Clients C

- Voice Broker VB

- Dealers D

- Electronic Broker EB

- Prime Broker PB

- Retail Aggregator – RA

- Multi Bank Trading – MBT

- Single Bank Trading – SBT

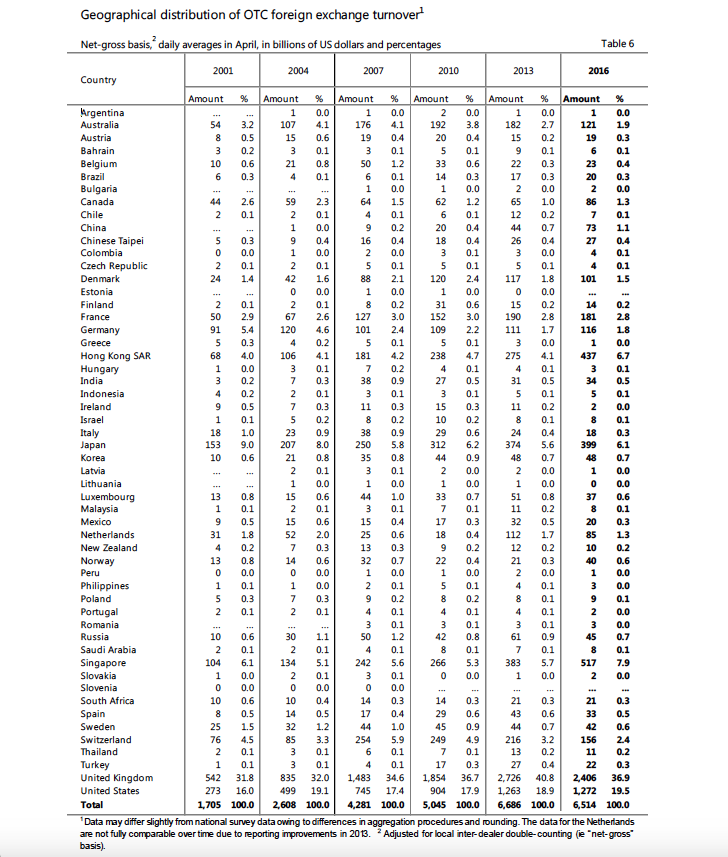

Top 10 FX Turnover Locations

- United Kingdom – 37%

- United States – 20%

- Singapore – 7.9%

- Hong Kong SAR – 6.7%

- Japan – 6.1 %

- France – 2.8%

- Switzerland – 2.4%

- Australia – 1.9%

- Germany – 1.8%

- Canada – 1.3%

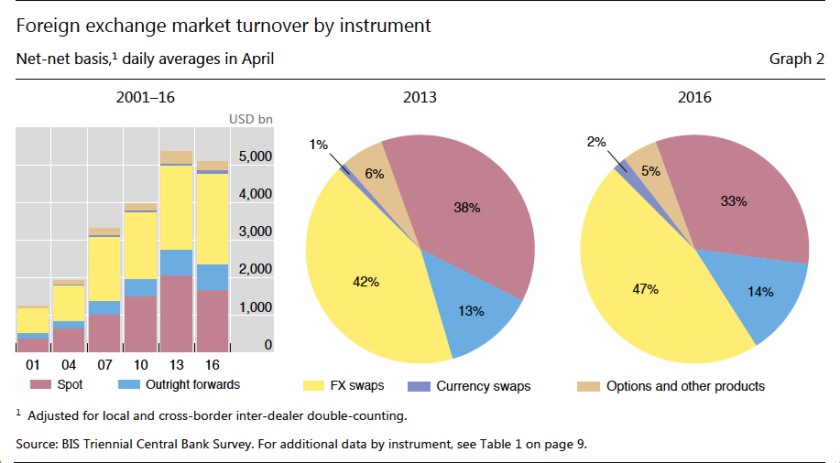

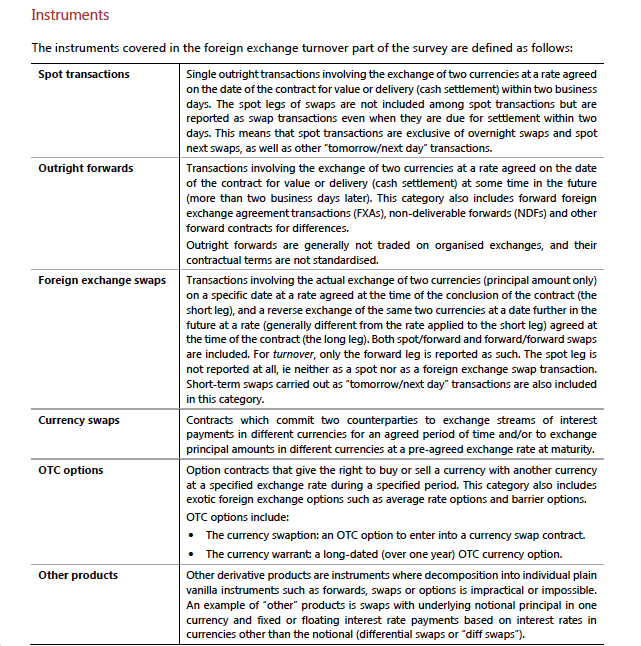

FX Instruments

- Spot

- FX Swap

- Outright Forward

- Currency Swaps

- FX Options

Currencies and Currency Pairs

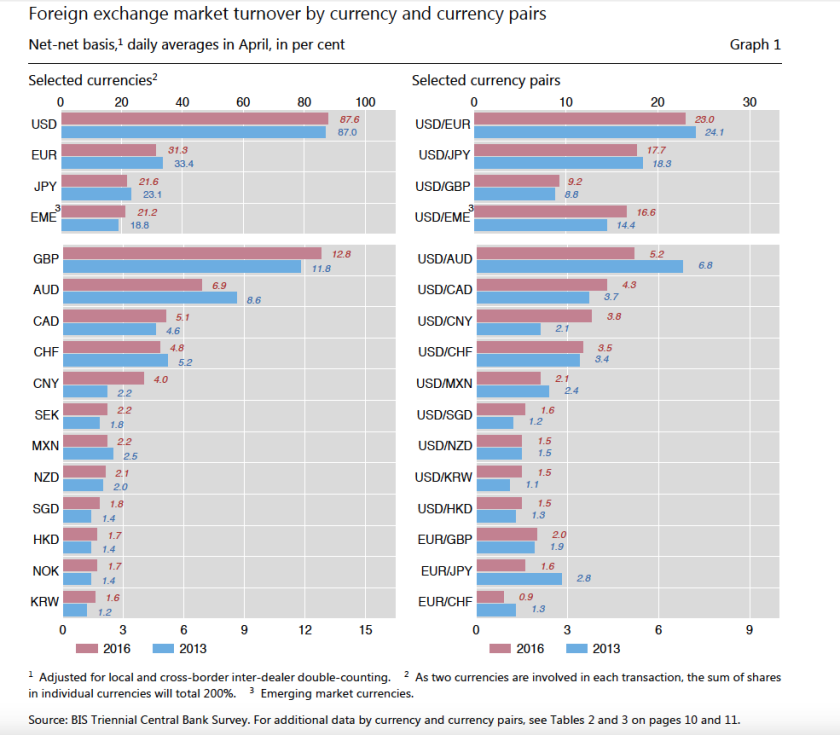

US Dollar is the king in FX market. 87.6% of transactions include USD on one side of currency pair. Euro comes at second with 31%. Japanese Yen is at 21.6%. UK Pound Sterling is at 12.8%. Chinese Yuan has moved to 4%.

Currencies and Currencies Pairs

Trends in FX Market

- Electronic Trading

- Algorithmic Trading

- High Frequency Trading

- Non Bank Liquidity Providers (Market Makers)

Non Bank Electronic Market Makers

The diverse set of non-bank electronic market-makers includes

- XTX Markets

- Virtu Financial

- Citadel Securities

- GTS

- Jump Trading.

These market-makers’ trading volume is captured in the Triennial because their trades are prime-brokered by a dealer bank. They are active on multilateral trading platforms, where they provide prices to banks’ e-trading desks, retail aggregators, hedge funds and institutional clients.

Chinese RMB – in FX Markets

- Second in Trade Finance

- Sixth in Payments

- Eighth in FX Trading

Considering China’s Renminbi for International Settlement and Forex Trading

On October 1, 2016, the International Monetary Fund added China’s renminbi1 (RMB) to its elite Special Drawing Right (SDR) basket of currencies, alongside the U.S. dollar, euro, yen and British pound. IMF said the change reflected China’s progress in reforming its monetary, foreign exchange and financial systems, and improving its financial market infrastructure.2 Short-term, this means countries can now include RMB assets in official FX reserves, making it easier for them to meet IMF guidelines.3 Beyond this, however, inclusion in SDR is a symbol of RMB’s emergence as an international currency for forex trading and settlement of global business transactions.

RMB’s ongoing progress is an important consideration for businesses involved in any FX trading, and particularly for those whose business or currency trading activities involve China.

RMB Usage Grows in Trade and Currency Trading

IMF’s decision arrives in the context of growing RMB usage in trade finance, international payments, and forex trading. In trade finance, RMB is now second amongst world currencies, reflecting enormous international trade with China.4

Since 2013, according to the Society for Worldwide Interbank Financial Telecommunication’s (SWIFT’s) monthly Renminbi Tracker, China’s currency has risen from ninth to fifth worldwide in total payments sent and received by value, not counting payments by central banks. During that period, it surpassed the Swedish Krona (SEK), Canadian Dollar (CAD), Swiss Franc (CHF), Australian Dollar (AUD) and, briefly during summer 2015, even the yen (JPY). RMB use is growing slowly in some markets (such as France, Switzerland and Germany), and is rapidly accelerating in others (e.g., the United Arab Emirates).5 SWIFT has elsewhere reported that 50 countries now use RMB for 10 percent or more of their trade with China.6

Meanwhile, according to the Bank for International Settlements’ (BIS’) September 2016 Central Bank Survey, RMB has doubled its share of OTC currency trading transactions since 2013. It has surpassed Mexico’s peso to become the most active developing market currency on forex trading exchanges, and is now eighth in FX trading amongst all currencies worldwide. BIS’s report notes that “as much as 95 percent of renminbi trading volume was against the U.S. dollar.”7

Building the Global Infrastructure for an Internationalized Currency

To promote RMB usage abroad, the People’s Bank of China (PBOC) – China’s central bank – has authorized 18 new official clearing banks worldwide since December 2012. These have opened in locations including Toronto, Buenos Aires, London, Paris, Johannesburg, Sydney, Seoul and Taipei.8 In September 2016, PBOC announced the first RMB clearing and settlement services in the U.S.9

Domestically, China has eliminated a cap on the number of enterprises permitted to carry out cross-border RMB settlements. Any company permitted to engage in import-export business may settle in RMB, unless it appears on a “black name list” (in which case its transactions may be reviewed individually).10 Restrictions have also been relaxed on RMB-denominated investments by foreigners.11

As Yu Yongding of the Asian Development Bank Institute has pointed out, China is the only country that has ever decided on its own to make internationalizing its currency a national priority.12 In determining how far RMB’s internationalization will go, China’s authorities appear to be balancing the benefits and risks of liberalization,13 carefully timing their decisions accordingly.

They face significant obstacles, not least the continuing downward pressure on the value of China’s currency on forex trading exchanges since it peaked against the U.S. dollar in early 2014. Some market observers believe RMB faces bank sector headwinds that might require a government bailout,14 as well as increased protectionist pressures in the U.S.15 and elsewhere. If these events lead to further reductions in RMB’s value, China could face accelerating capital flight,16 deepening internal opposition to the full elimination of capital controls.

Transacting in RMB

China’s reforms have made it easier for companies that do business in China to settle their transactions in RMB if they so desire. Many of their Chinese trading partners would welcome this, and some may even offer discounts if they can invoice in RMB.17 China’s central bank has estimated that transacting in U.S. dollars may add 2-to-3 percent in administrative expenses alone.18

The risk of currency fluctuation, however, remains a significant issue. Hedging vehicles exist; of course, these have their own costs. In making the decision about whether to transact business in RMB or another currency, companies may wish to make careful and timely assessments about currency risk.

The Takeaway

As China’s financial and market reforms move forward, RMB is emerging as a leading international currency. It has become far easier for international businesses and currency traders to transact in China’s home currency. International businesses may wish to carefully consider currency risk in developing their own plans for RMB forex trading and settlement.

Key Terms:

- PB (Prime Brokerages)

- Inter Dealer

- Multi Dealer Trading

- Single Dealer Trading

- HFT (High Frequency Trading)

- Market Makers

- Liquidity Providers

- Retail Aggregators

- Retail FX Systems

- Algorithmic Trading

- FX ECNs (Electronic Communication Networks)

- e-Trading

- Hedge Funds

- Institutional Clients

- Non Bank Liquidity Providers

- FXPB (Foreign Exchange Prime Brokerage)

Key Sources of Research:

Buttonwood The financial markets in an era of deglobalisation

Why the global volume of foreign-exchange trading is shrinking

Dec 15th 2016

Downsized FX markets: causes and implications

BIS

Triennial Central Bank Survey Foreign exchange turnover in April 2016

TheForeign Exchange andInterest Rate Derivatives Markets:Turnover in the United States, April 2016

The foreign exchange and over-the-counter interest rate derivatives market in the United Kingdom

Quarterly Bulletin 2016 Q4

16 December 2016

By Alexander Hutton and Edward Kent

http://www.bankofengland.co.uk/publications/Pages/quarterlybulletin/2016/q4/a6.aspx

The anatomy of the global FX market through the lens of the 2013 Triennial Survey

The foreign exchange and over-the-counter interest rate derivatives market in the United Kingdom

2013

The $4 trillion question: what explains FX growth since the 2007 survey?

CME Group OTC FX Clearing

Click to access otc-fx-clearing.pdf

CME Group Cleared OTC Financial Products

Click to access cleared-otc-financial-products.pdf

Citi tops Euromoney global FX poll again, but big banks lose grip

http://www.reuters.com/article/global-forex-euromoney-idUSL5N18M29O

Foreign Exchange Market

https://en.wikipedia.org/wiki/Foreign_exchange_market

All change in the 2016 Euromoney FX rankings

World’s Best FX Providers 2017

Automation, “algo trading” and a tighter regulatory environment are driving change in the industry

https://www.gfmag.com/topics/blogs/it-pays-have-good-forex-bank

360T

http://www.360t.com/about-us/press/

CBOE Will Acquire BATS Global Markets for $3.2 Billion

http://fortune.com/2016/09/26/cboe-acquires-bats/

e-FOREX

http://www.e-forex.net/institutional-fx-ecommerce.html

Providing Differentiated Service in an Ever-Evolving Market

2016 Greenwich Leaders: Global Foreign Exchange Services

https://www.greenwich.com/fixed-income-fx-cmds/providing-differentiated-service-ever-evolving-market

Press Release: Best FX Awards 2017 – Providers and Corporate

https://www.gfmag.com/media/press-releases/best-fx-awards-2017-providers-and-corporate

Global Finance Names The World’s Best Foreign Exchange Providers 2016

Global Banking & Finance Review Awards – 2015

https://www.globalbankingandfinance.com/global-banking-finance-review-awards-2015/

Click to access Rime%20New%20Electronic%20FX1.pdf

Foreign exchange market structure, players and evolution

Michael R. King, Carol Osler and Dagfinn Rime

2011

Settlement Risk in the Global FX Market: How Much Remains?

8 Nov 2016

Dino Kos

Richard M. Levich

https://papers.ssrn.com/sol3/papers2.cfm?abstract_id=2827530

The Retail Spot Foreign Exchange Market Structure and Participants

John H. Forman III

March 22, 2016

https://papers.ssrn.com/sol3/papers2.cfm?abstract_id=2753823

Algorithmic trading in the foreign exchange market

Maria Bergsten and Johannes Forss sandahl

2013

Click to access rap_pov_artikel_2_130321_eng.pdf

The Future of the Foreign Exchange Market

Richard K. Lyons

Click to access Lyons%20Brookings.pdf

Multi Bank Platforms

http://www.londonfx.co.uk/ecn.html

ECNs/Alternative Trading Systems

https://www.sec.gov/divisions/marketreg/mrecn.shtml

The Transition to Electronic Communications Networks in the Secondary Treasury Market

Bruce Mizrach and Christopher J. Neely

http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.205.6479&rep=rep1&type=pdf

Deal or no deal: anatomy of an FX portal

http://treasurytoday.com/2013/06/deal-or-no-deal-anatomy-of-an-fx-portal

The 3 Pillars of Forex

http://www.zerohedge.com/news/2016-06-11/3-pillars-forex

THE VALUE OF APAMA

IN FAST-CHANGING FX MARKETS

Click to access sec_SAG_Apama_In-Fast-Changing-FX-Markets_4PG_WP_Feb16_tcm16-116205.pdf

The Global Foreign Exchange Market: Growth and Transformation

William Barker

FX ALL

Currenex

Most Innovative Bank e-FX Trading Platform: Citi

http://www.fxweek.com/fx-week/interview/2464092/most-innovative-bank-e-fx-trading-platform-citi#

Citi sells its electronic FX platform

https://ftalphaville.ft.com/2010/01/04/118946/citi-sells-its-electronic-fx-platform/

Nasdaq poised to launch FX trading platform: top executive

http://www.reuters.com/article/us-nasdaq-forex-idUSKCN0QT1VD20150824

State Street buys electronic foreign exchange trading platform Currenex

EBS

Electronic Platforms in Foreign Exchange Trading

http://celent.com/reports/electronic-platforms-foreign-exchange-trading

HOTSPOT FX

Icap’s EBS BrokerTec Inks Deal With China’s CFETS

Best Single-Dealer FX Trading Platform

Multi-Dealer Platforms to gain ground in 2015

http://www.e-forex.net/articles/apr-2015-multidealer-platforms-to-gain-ground-in-2015.html

PERSPECTIVE ON NEW ELECTRONIC PLATFORMS, FROM EXECUTION TO DISTRIBUTION

http://fintank.net/position_papers/electronic_platforms/

FX Trading Platforms: Models Converge and Competition Heats Up

http://celent.com/reports/fx-trading-platforms-models-converge-and-competition-heats

Trends in Foreign Exchange Markets and the Challenges Ahead

https://www.newyorkfed.org/newsevents/speeches/2015/pot150714

Restoring trust in global FX markets

Click to access restoring-trust-report.pdf

2016 – Entering the Age of the “Non-Bank”

The New Wall Street: Even Big Banks Want Help Navigating Markets

Matthew Leising and Annie Massa

Aug 10, 2016

http://www.wealthmanagement.com/markets/new-wall-street-even-big-banks-want-help-navigating-markets

The Future of Computer Trading in Financial Markets

An International Perspective

Click to access tacfuturecomputertrading1012.pdf

Small Fish Big Prize: Market Makers out to eat Bank’s lunch

Click to access Small-fish-big-prize-The-Market-makers-out-to-eat-the-banks.pdf

Automated Trading in Treasury Markets

Click to access TMPG%20HFT%20White%20Paper%20FINAL%20-%202015-04-08.pdf

High Frequency Traders Elbow Their Way Into the Currency Markets

by Lananh Nguyen

September 12, 2016

Exclusive: U.S. investigates market-making operations of Citadel, KCG

http://www.reuters.com/article/us-usa-stocks-probe-exclusive-idUSKCN0Y11CJ

Considering China’s Renminbi for International Settlement and Forex Trading

By Bill Camarda

https://www.americanexpress.com/us/content/foreign-exchange/articles/renminbi-for-forex-trading/

Pound plummet blamed on ‘liquidity holes’

Sterling’s flash crash was triggered during Asian ‘graveyard shift’ when US/European traders away

https://www.ft.com/content/dc7c0846-8e00-11e6-a72e-b428cb934b78

CLS Bank